Working tax credit

Eligibility

You can only make a claim for Working Tax Credit if you already get Child Tax Credit.

If you cannot apply for Working Tax Credit, you can apply for Universal Credit instead.

You might be able to apply for Pension Credit if you and your partner are State Pension age or over.

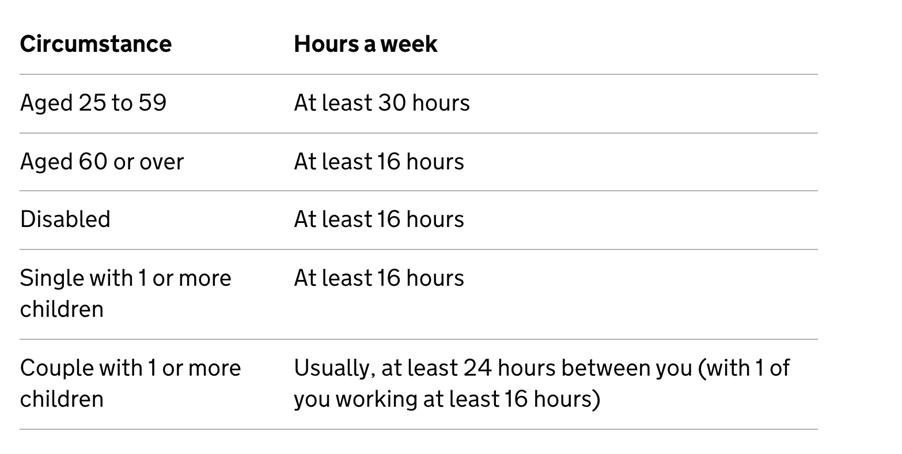

Hours you work

You must work a certain number of hours a week to qualify.

A child is someone who is under 16 (or under 20 if they’re in approved education or training).

You can still apply for Working Tax Credit if you’re on leave.

Exceptions for couples with at least one child

You can claim if you work less than 24 hours a week between you and one of the following applies:

- you work at least 16 hours a week and you’re disabled or aged 60 or above

- you work at least 16 hours a week and your partner is incapacitated (getting certain benefits because of disability or ill health), is entitled to Carer’s Allowance, or is in hospital or prison

What counts as work

Your work can be:

- for someone else, either as their employeeor as a worker

- as someone who’s self-employed

- a mixture of the two

If you’re self-employed

Some self-employed people are not eligible for Working Tax Credit. To qualify, your self-employed work must aim to make a profit. It must also be commercial, regular and organised.

This means you may not qualify if you do not:

- make a profit or have clear plans to make one

- work regularly

- keep business records, such as receipts and invoices

- follow any regulations that apply to your work, for example having the right licence or insurance

If the average hourly profit from your self-employed work is less than the National Minimum Wage, HM Revenue and Customs may ask you to provide:

- business records

- your business plan – find out how to write a business plan

- details of the day-to-day running of your business

- evidence that you’ve promoted your business – such as advertisements or flyers

Your pay

The work must last at least 4 weeks (or you must expect it to last 4 weeks) and must be paid.

This can include payment in kind (for example farm produce for a farm labourer) or where you expect to be paid for the work.

Exceptions

Paid work does not include money paid:

- for a ‘Rent a Room’ scheme(less than £7,500 or £3,750 for joint owners)

- for work done while in prison

- as a grant for training or studying

- as a sports award

Your income

There’s no set limit for income because it depends on your circumstances (and those of your partner). For example, £18,000 for a couple without children or £13,100 for a single person without children – but it can be higher if you have children, pay for approved childcare or one of you is disabled.

CHILD TAX CREDIT

Overview

You can only make a claim for Child Tax Credit if you already get Working Tax Credit.

If you cannot apply for Child Tax Credit, you can apply for Universal Credit instead.

You might be able to apply for Pension Credit if you and your partner are State Pension age or over.

What you’ll get

The amount you can get depends on how many children you’ve got and whether you’re:

Child Tax Credit will not affect your Child Benefit.

You can only claim Child Tax Credit for children you’re responsible for.

For further information, please contact your usual Beavis Morgan Partner or email info@beavismorgan.com.